Planning for retirement through the National Pension System (NPS) requires one important decision at the time of account opening — choosing between active choice and auto choice in NPS. Both options are designed to help investors build a retirement corpus in a disciplined and tax-efficient manner, but they differ in terms of control, flexibility, and risk management.

If your goal is long-term tax-efficient growth, understanding how these two approaches work can help you make a smarter decision aligned with your financial goals.

What is Active Choice in NPS?

Active choice in NPS allows investors to decide how their contributions are allocated across different asset classes. It is a self-managed investment option that gives subscribers full control over portfolio distribution.

Under this approach, you can allocate your funds among:

- Equity (E) – Growth-oriented but volatile

- Corporate Debt (C) – Moderate risk

- Government Securities (G) – Low risk

The primary purpose of active choice in NPS is to empower investors who understand market dynamics and want to customize their retirement portfolio according to their risk appetite and financial strategy.

Key Features of Active Choice

- Full control over asset allocation

- Flexibility to adjust allocation (within regulatory limits)

- Maximum equity exposure up to 75% (till age 50)

- Suitable for experienced investors

- Requires periodic monitoring and rebalancing

Investors who are comfortable tracking markets and adjusting strategies may find active choice in NPS more rewarding over the long term.

What is Auto Choice in NPS?

Auto Choice is excellent for individuals who prefer a hands-off approach to investment strategy. It automatically allocates your contributions across different asset classes based on your age, with the aim of optimizing risk and return.

They provide a balanced approach to investment, gradually shifting from higher-risk equities to more stable debt instruments as the subscriber nears retirement.

The idea is simple:

- Higher equity allocation when you are young

- Gradual shift toward safer assets as you approach retirement

This automated rebalancing ensures that risk reduces over time without requiring active intervention from the investor.

Key Features of Auto Choice

Auto choice in NPS offers four lifecycle fund variants:

1. Aggressive Lifecycle Fund – Allowing 50% of equity allocation up to 45 years of age. The share reduces to 35% till the age of 55

2. High Lifecycle Fund (LC75) – Higher starting equity allocation of 75% till age 35 and further gets tapered to 15% till age 55

3. Moderate Lifecycle Fund (LC50) – Balanced approach where equity allocation remains 50% till age 35 and lowers to 10% by the age 55

4. Conservative Lifecycle Fund (LC25) – Equity exposure is lowest in this choice, it starts with 25% till 35 and further decreases to 5% by the age 55

Other key features include:

- Automatic portfolio rebalancing

- Age-based risk reduction

- No need for active monitoring

- Ideal for beginners and hands-off investors

For individuals who prefer simplicity and discipline, auto choice in NPS provides a structured and convenient solution.

Tax Benefits in Both Active Choice and Auto Choice

Tax benefits remain identical for both options because taxation depends on the NPS framework, not on the investment style.

During Investment:

- Section 80CCD(1): Deduction up to ₹1.5 lakh (within Section 80C limit)

- Section 80CCD(1B): Additional ₹50,000 exclusive deduction

- Section 80CCD(2): Employer contribution (additional benefit)

At maturity:

- 60% withdrawal is tax-free

- 40% must be used to buy an annuity (taxed as income when received)

Therefore, both active choice in NPS and auto choice in NPS offer equal tax efficiency.

Choosing Between Auto Choice and Active Choice

Deciding between Auto Choice and Active Choice largely depends on your financial literacy, risk tolerance, and investment goals. Here are a few considerations:

1. Risk Tolerance: If you’re risk-averse or lack investment experience, Auto Choice might be more suitable. Conversely, if you are comfortable with market fluctuations and have a good grasp of investing, Active Choice could yield better returns.

2. Time Commitment: Auto Choice requires minimal involvement, making it ideal for busy professionals. If you enjoy following the markets and can dedicate time to managing your investments, Active Choice might be rewarding.

3. Financial Goals: Consider your retirement goals. If you want to maximize your corpus, Active Choice can be advantageous. However, if you prefer a balanced approach that gradually reduces risk, Auto Choice may align better with your objectives.

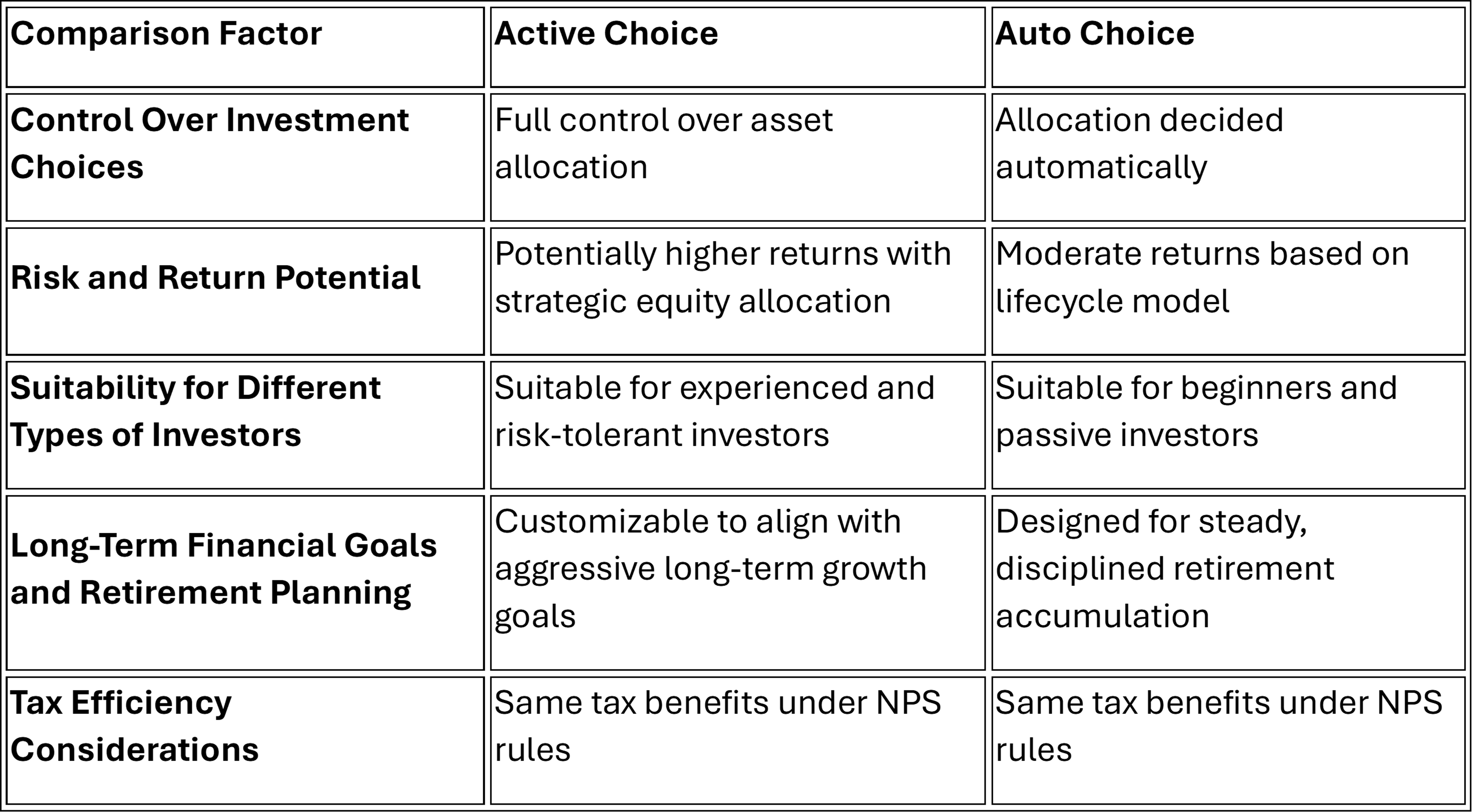

Active Choice vs Auto Choice in NPS: A Direct Comparison

Final Verdict: Which is Better for Long-Term Tax-Efficient Growth?

There is no universally superior option between active choice in NPS and auto choice in NPS. The right choice depends on your financial knowledge, time commitment, and risk tolerance.

Choose Active Choice if:

- You understand asset allocation.

- You want higher equity exposure in early years.

- You are comfortable managing investments actively.

Choose Auto Choice if:

- You prefer automation.

- You want disciplined risk reduction.

- You do not wish to monitor markets regularly.

For long-term tax-efficient growth, consistency, early investing, and disciplined contributions matter more than the selection itself. Both options provide identical tax benefits — the difference lies in control and flexibility.

Frequently Asked Questions

Can I switch between Active Choice and Auto Choice in NPS?

Yes, NPS allows subscribers to switch between active choice and auto choice. This flexibility helps investors adapt their strategy as their financial knowledge or risk appetite changes.

Which option offers better returns in NPS: Active Choice Vs. Auto Choice?

Active choice may offer higher returns if managed strategically with optimal equity allocation. However, auto choice can provide stable growth through disciplined lifecycle rebalancing. Returns ultimately depend on asset allocation and market conditions.

Auto Choice Vs. Active Choice in terms of risk?

Auto choice is generally considered safer because it automatically reduces equity exposure with age. Active choice can carry higher risk if aggressive allocations are maintained without proper monitoring.

How do tax benefits differ between Active Choice and Auto Choice in NPS?

There is no difference in tax benefits. Both active choice and auto choice qualify for the same deductions and tax treatment under NPS rules.

Which choice should I pick for tax savings in the long run?

Since tax benefits are identical, your decision should depend on your investment style. If you prefer control, choose active choice. If you prefer automation and discipline, auto choice may be the better option for long-term retirement planning.

Disclaimer

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns under NPS are subject to market risk and are prone to fluctuation depending on the state of the Financial market.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the schemes of DSP Pension Fund Managers Private Limited. Tax laws are subject to change.