What is NPS Contribution?

The National Pension System (NPS) is a government-backed, voluntary retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Launched in 2004 for central government employees and opened to all Indian citizens in 2009, NPS has grown into one of the most tax-efficient and flexible retirement vehicles available in India today.

An NPS contribution refers to the money a subscriber deposits into their NPS account — either voluntarily or as part of a structured employer-employee arrangement. These contributions are invested across asset classes including equities (E), corporate bonds (C), and government securities (G), depending on the subscriber's chosen investment strategy. The accumulated corpus grows over the subscriber's working life and is used at retirement to fund both a lump sum payout and a regular monthly pension through annuity purchase.

What makes NPS contribution particularly meaningful is not just the retirement wealth it builds, but the triple layer of tax benefits it offers — benefits unavailable in most other savings instruments. Understanding what NPS contribution means, how it works, and how much to invest is essential for anyone serious about financial planning in India.

Key Takeaways about NPS Contributions

• NPS contributions can be made by salaried employees, self-employed professionals, and NRIs between the ages of 18 and 85.

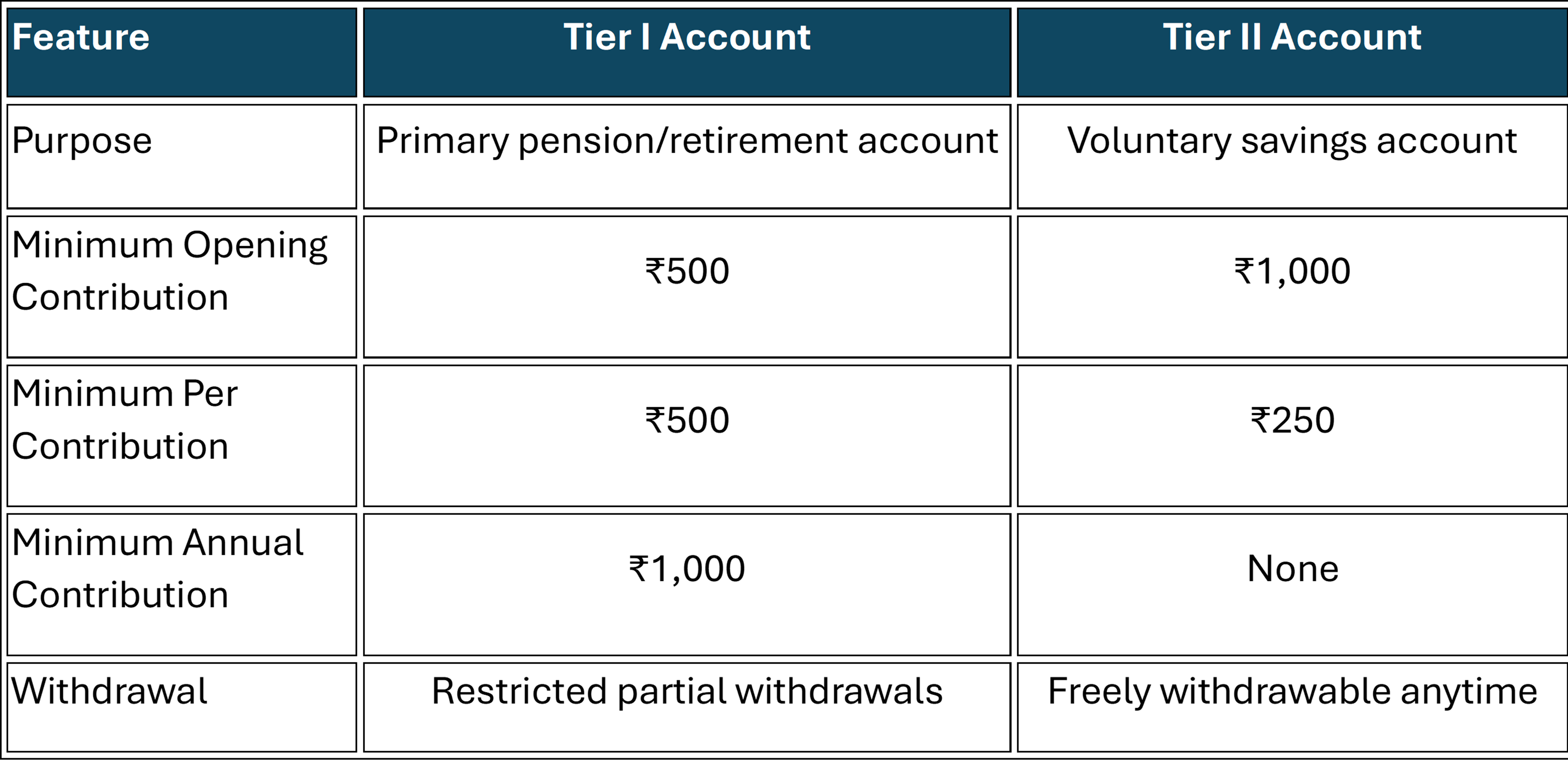

• There are two account types: Tier I (pension account with lock-in) and Tier II (voluntary savings with no lock-in).

• The minimum NPS contribution for Tier I is ₹500 per contribution and ₹1,000 per year; for Tier II, it is ₹250 per contribution.

• Subscribers can claim up to ₹2 lakh in tax deductions annually — ₹1.5 lakh under Section 80CCD(1) within the 80C limit, and an additional ₹50,000 under Section 80CCD(1B).

• Employer contributions under Section 80CCD(2) offer additional tax deductions with no upper cap within salary limits.

• At maturity, 60% of the corpus is paid as a tax-free lump sum; 40% must be used to buy an annuity.

• Contributions can be made online via the CRA portal through net banking, or UPI, and offline through Point of Presence (PoP) service providers such as banks.

Who Can Contribute to NPS?

NPS is open to a broad spectrum of individuals, making it one of the most inclusive retirement platforms in India. Any Indian citizen between the age of 18 and 85 years — whether salaried or self-employed — can open an NPS account and begin making contributions.

Salaried employees working in the private sector can enrol individually or through their employer under the Corporate NPS model. Central and state government employees are mandatorily enrolled in NPS (for those who joined service after January 1, 2004). A government employee and their employer each contribute 10% of Basic Pay + Dearness Allowance, while central government employees receive a 14% employer contribution.

Self-employed individuals such as doctors, lawyers, freelancers, and business owners are equally eligible. They contribute entirely on their own and can claim deductions of up to 20% of gross income under Section 80CCD(1).

Non-Resident Indians (NRIs) are also permitted to contribute to NPS, subject to FEMA guidelines, as long as they hold a valid Indian bank account. OCIs (Overseas Citizens of India), are also eligible to open an NPS account.

For example, a 32-year-old software engineer earning ₹18 lakh annually, a 45-year-old self-employed chartered accountant, and a 28-year-old NRI working in Dubai can all open NPS accounts and make regular contributions — each benefiting from tax savings and long-term wealth creation.

Minimum Contribution Required for NPS

The minimum NPS contribution requirements differ between the two account types and are designed to keep the barriers to entry low while ensuring account activity.

For a Tier I account, the minimum contribution at the time of account opening is ₹500. Going forward, each individual contribution must be at least ₹500, and the subscriber must make a minimum total contribution of ₹1,000 in a financial year to keep the account active. If contributions fall below this threshold, the account is "frozen" and must be reactivated by paying the minimum due amount along with a penalty of ₹100 per year of default.

For a Tier II account, the minimum opening contribution is ₹1,000, and subsequent contributions must be at least ₹250 each. There is no mandatory annual minimum for Tier II accounts, and the account can remain dormant without penalty.

To illustrate: if you open a Tier I NPS account today with ₹500 and subsequently make two contributions of ₹500 in the same financial year, you have met the minimum requirement. However, most financial planners advise contributing significantly more — ideally ₹50,000 per year at the minimum — to make meaningful use of the 80CCD(1B) tax deduction and build a substantial corpus over time.

Difference Between NPS Tier 1 and Tier 2 Contributions

The Tier I account is the core retirement vehicle and is where the power of NPS — both in terms of long-term compounding and tax efficiency — truly lies. The Tier II account functions more like a liquid mutual fund and is best used for shorter-term financial goals.

How to Make NPS Contributions Online

Contributing to NPS online is simple and can be done through the official eNPS portal or through the PoP platform.

Here are the steps:

- Visit the CRA portal at depending on PRAN association.

- Click on "Contribution" on the homepage.

- Enter your PRAN (Permanent Retirement Account Number) and password.

- Select the account type — Tier I or Tier II.

- Enter the contribution amount (minimum ₹500 for Tier I).

- Choose your payment method: net banking, debit card, or UPI.

- Complete the payment through your bank's gateway.

- A transaction confirmation and receipt will be generated and emailed to the subscriber.

How to Make NPS Contributions through Direct Remittance

Subscribers who want to get the NAV of same day can make contribution through Direct Remittance of NPS

- Register for D- Remit by login to your NPS account. Select whether you want do it for Tier 1, Tier 2 or both.

- You will get the virtual account number along with the steps to follow on email post the registration.

- Add new payee details in your bank account as indicated in the email

- Make the contribution by transferring money to the new NPS payee account to get the NAV of same day

- Collect the acknowledgment receipt with a transaction number for your records

What Is the Employer Contribution Rule in NPS?

Under the Corporate NPS model, employers can contribute to their employees' NPS accounts, and this arrangement comes with one of the most generous tax benefits in the Indian tax code. The employer's NPS contribution — up to 10% of Basic Salary plus Dearness Allowance under old tax, and up to 14% under new tax regime — is deductible under Section 80CCD(2) of the Income Tax Act. Critically, this deduction is available over and above the ₹1.5 lakh limit under Section 80C and the additional ₹50,000 under Section 80CCD(1B), meaning it sits entirely outside the usual tax-saving ceiling.

From the employee's perspective, the employer's NPS contribution does not form part of their taxable income allowing superior retirement savings without extra personal outflow. For example, if an employee has a Basic Salary of ₹60,000 per month (₹7.2 lakh per year), an employer contributing 10% to NPS adds ₹72,000 to the retirement corpus annually — fully tax-free in the employee's hands.

Companies can register for Corporate NPS through any PoP empaneled by PFRDA. Employees of registered corporates can also contribute voluntarily over and above the employer's share.

NRI Contribution in NPS: Rules and Process

NRIs and OCI are permitted to invest in NPS under the regulations framed by PFRDA, provided they meet certain conditions.

NRI contributions must be routed through an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) bank account held with an Indian bank.

For example, an Indian software professional working in Singapore on an Indian passport can open an NPS account online via eNPS using their NRE account, make contributions in Indian Rupees, and claim tax benefits as per prevalent rules.

Tax Benefits of NPS Contribution

NPS offers a three-layered tax advantage that is arguably unmatched by any other investment product in India:

• Section 80CCD(1): Contributions up to 10% of salary (for salaried) or 20% of gross income (for self-employed) are deductible, subject to a combined 80C ceiling of ₹1.5 lakh. This means NPS competes with PPF, ELSS, and life insurance within the same tax bucket.

• Section 80CCD(1B): An exclusive additional deduction of ₹50,000 per year for NPS contributions — entirely separate from and on top of the ₹1.5 lakh 80C limit. A taxpayer in the 30% bracket saves ₹15,600 in tax annually from this deduction alone.

• Section 80CCD(2): Employer's NPS contributions up to 10% or 14% of Basic + DA are fully deductible under this section — and do not count toward the 80C or 80CCD(1B) limits.

• At exit: 60% of the total NPS corpus withdrawn as a lump sum at age 60 is entirely tax-free. The annuity income received thereafter is taxable as per the subscriber's applicable income slab.

Charges on NPS Contribution

NPS is one of the lowest-cost retirement products in the world, but it is not entirely free of charges. Here is an overview of the key fees:

PoP fee is capped at 0.2% annually. Pension Fund Managers (PFMs) who invest your corpus charge an annual fund management fee upto 0.12% of AUM — extraordinarily low compared to mutual funds. The NPS Trust also charges a nominal custodian fee. Together, the total cost of running an NPS account is typically well low per year, making it among the most cost-efficient investment vehicles in India.

How to Check NPS Contribution Statements Online

• Log in to the CRA (Central Recordkeeping Agency) portal using your PRAN and IPIN (password).

• On the dashboard, click on "Transaction Statement" under the "View" menu.

• Select the financial year or a custom date range for which you need the statement.

• Choose Tier I, Tier II, or both.

• Click "Generate" to view the statement on screen, or click "Download" to save it as a PDF.

• The statement shows all contributions made (including employer contributions if applicable), NAV at the time of contribution, number of units allotted, and the current value of your holdings.

Alternatively, you can download the NPS app and access the same statement from your mobile. Contribution statements can also be emailed automatically each quarter if you have registered your email with the CRA.

What Happens If I Stop Making NPS Contributions?

If a subscriber fails to make the minimum required NPS contribution of ₹1,000 per year in a Tier I account, the account is classified as "frozen." A frozen account cannot be operated — no new contributions, no withdrawals, and no changes to fund allocation or nomination. To reactivate the account, the subscriber must visit their PoP-SP, submit a reactivation request, and pay the minimum contribution to activate the PRAN.

It is important to understand that stopping contributions does not mean the existing corpus is lost. Your previously invested amount continues to stay invested in the chosen fund and will grow (or fluctuate) based on market performance. However, the compounding effect slows significantly when fresh contributions cease, and the gap in retirement corpus can be substantial.

For individuals who go through periods of financial difficulty, it is advisable to contribute even a small amount — ₹1,000 to ₹2,000 per year — to keep the account active rather than letting it freeze. The long-term cost of interruption, particularly in the early years when compounding has the most impact, is far greater than the cost of maintaining minimum contributions.

How Much Should You Contribute to NPS to Receive ₹50,000 Pension?

To receive a monthly pension of ₹50,000 through NPS annuity, you need to work backwards from the annuity rates and corpus requirement. Assuming an annuity rate of 6% per annum, you would need a monthly pension of ₹50,000 (₹6 lakh per year), and since 40% of your NPS corpus is mandatorily used to buy the annuity, the calculation looks like this:

Annuity corpus required: ₹6,00,000 ÷ 6% = ₹1 crore. Since this represents 40% of the total corpus, the total NPS corpus needed at retirement = ₹1 crore ÷ 0.40 = ₹2.5 crore.

To build a corpus of ₹2.5 crore over 30 years (investing from age 30 to 60) at an assumed return of 10% per annum on a balanced NPS portfolio, the required monthly SIP contribution would be approximately ₹13,500 per month or ₹1.62 lakh per year.

This is precisely why the rule of thumb that your NPS contribution should be 9 to 10 times your monthly salary is such a powerful guideline. If your monthly salary is ₹50,000, contributing 9–10x, i.e., ₹4.5 lakh to ₹5 lakh annually (spread monthly), will — over a 25–30 year horizon — build a corpus substantial enough to support a meaningful monthly pension without dependence on other income sources.

The earlier you start, the lower the monthly amount needed. A 25-year-old needs to invest roughly ₹8,000–₹9,000 per month to reach ₹2.5 crore by 60. A 40-year-old would need to invest ₹40,000+ per month to achieve the same goal. Time is the greatest variable in NPS contribution planning.

Frequently Asked Questions (FAQs)

Q1. Is NPS paid monthly?

No, NPS contributions are not mandatorily monthly — you can contribute at any frequency you choose, as long as the minimum annual threshold of ₹1,000 is met for Tier I accounts.

Q2. Can I withdraw 100% from NPS?

yes, you cannot withdraw 100% of your NPS corpus at maturity if your total corpus is less than ₹8 lakh.

Q3. Is NPS 100% safe?

NPS is regulated by PFRDA and backed by the Government of India, making it a highly credible and well-governed retirement platform. However, it is not 100% capital guaranteed in the way a bank fixed deposit is. The returns depend on market performance, particularly the equity allocation. The government securities (G) fund is the safest option but offers lower returns. Over long horizons, the diversified NPS portfolio has historically delivered stable, inflation-beating returns. For risk-averse investors, choosing higher G and C allocation with minimal E provides near-safety with moderate returns.

Q4. Why is NPS not a good investment?

While NPS has many strengths, there are a few limitations worth considering. First, the mandatory annuity requirement — 40% of the corpus must go into an annuity at retirement — can be a disadvantage, since annuity rates in India are typically low (5–7%) and the income is fully taxable.

Second, the lock-in of funds limits liquidity for emergencies (though partial withdrawals are allowed 4 times for specific purposes). So NPS is less suitable for investors who prefer liquidity before retirement. It works best as one component of a broader retirement strategy rather than the sole vehicle

Disclaimer

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns under NPS are subject to market risk and are prone to fluctuation depending on the state of the Financial market.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the schemes of DSP Pension Fund Managers Private Limited. Tax laws are subject to change.