")

What is the National Pension System (NPS)?

The National Pension System (NPS) is a government-sponsored, voluntary retirement savings scheme launched by the Government of India to help citizens build a secure financial corpus for their retirement years. Introduced in January 2004 for central government employees and subsequently opened to all Indian citizens in 2009, the NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It is one of the most structured and transparent pension instruments available in India today.

At its core, understanding what is NPS means recognizing it as a defined contribution plan — meaning the retirement corpus depends on the amount contributed and the returns generated on those contributions over the years. The scheme is designed to instill a habit of saving for retirement while offering flexibility in investment choices and fund managers. Whether you are a salaried professional, a self-employed individual, or a government employee, the NPS caters to a wide range of investors seeking long-term financial security.

What is national pension system in terms of its governing structure? The NPS is overseen by PFRDA, which ensures that the funds are managed by registered Pension Fund Managers (PFMs) in a transparent and regulated manner. The scheme is also one of the lowest-cost pension plans globally, with minimal fund management charges, making it a cost-effective option for retirement planning.

How Does NPS Work?

Understanding how NPS functions is essential before making an investment decision. The scheme operates through a series of well-defined stages:

• Contribution: Subscribers open an NPS account and make regular contributions throughout their working life. There is no fixed contribution frequency — you can contribute monthly, quarterly, or annually based on your convenience.

• Investment: The contributions are invested in a mix of asset classes — equities (E), corporate bonds (C), and government securities (G). Subscribers can choose between Active Choice (self-directed allocation) or Auto Choice (age-based allocation).

• Fund Management: PFRDA-registered Pension Fund Managers like DSP Pension manage the contributions. There are ten Pension Fund Managers registered in NPS

• Accumulation Phase: Over the years, the corpus grows based on market-linked returns. The longer you stay invested, the greater the compounding benefit.

• Premature Exit: If you exit before superannuation, only 20% of the corpus can be withdrawn as a lump sum, and the remaining 80% must be annuitized. If the fund size is less then or equal to 5 lakh then full withdrawal can be done.

• Withdrawal/Exit: On reaching the age of 60, you can withdraw up to 60% of the corpus as a lump sum (tax-free), while the remaining 40% must be mandatorily used to purchase an annuity that provides a regular monthly pension. If the fund size is less then or equal to 8 lakh then full withdrawal can be done.

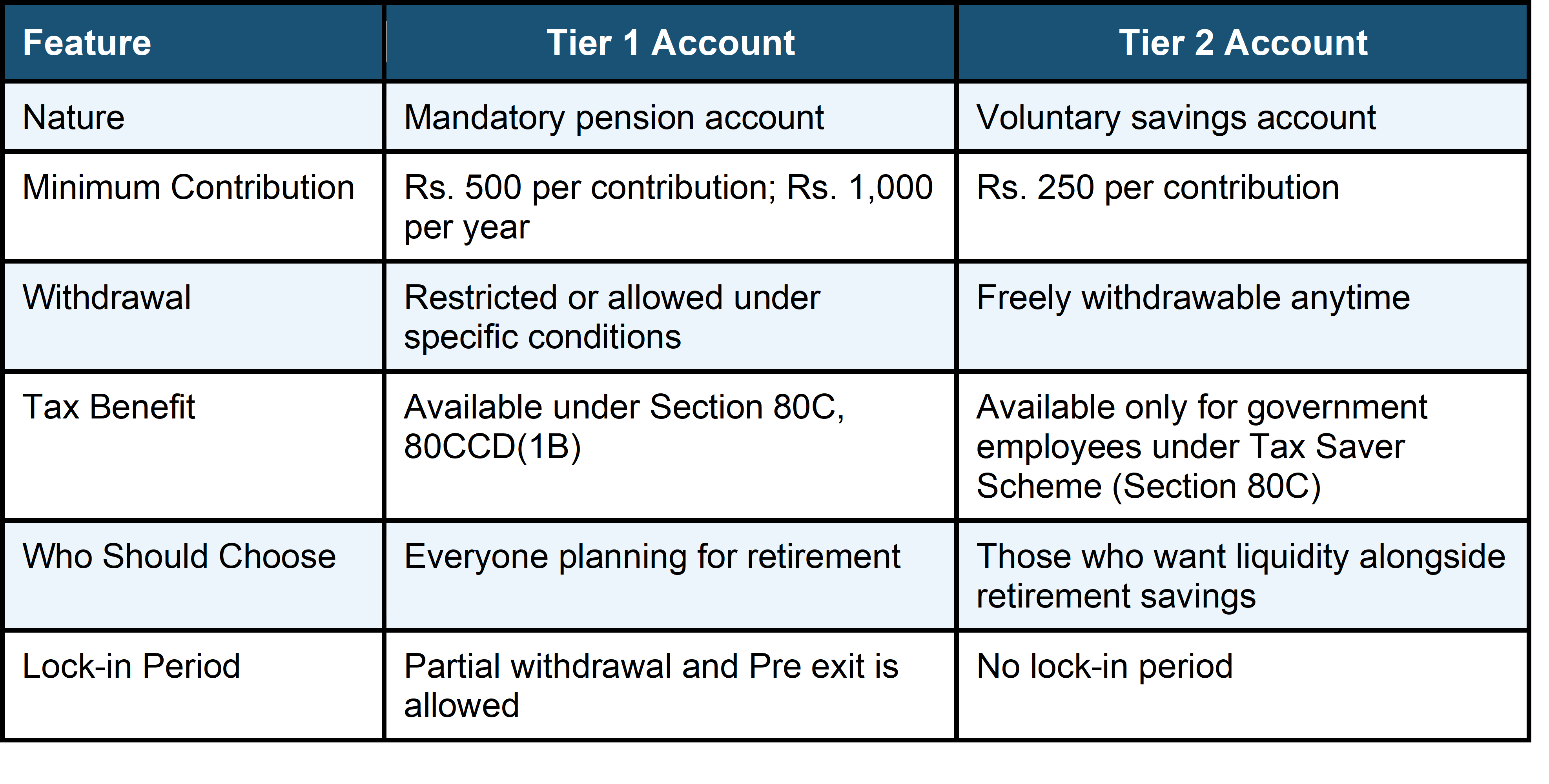

Types of NPS Accounts

The NPS offers two types of accounts — Tier 1 and Tier 2 — each designed to serve different financial needs and goals. Here is a comparative overview:

The Tier 1 account is the primary retirement account and is mandatory for NPS enrolment. The Tier 2 account, on the other hand, is an optional add-on that functions more like a savings account with the flexibility of free withdrawals.

Eligibility Criteria to Open NPS Account

The NPS is accessible to a broad spectrum of Indian citizens. Here are the key eligibility requirements:

Any Indian citizen — whether resident, non-resident (NRI), or Overseas Citizen of India (OCI) — between the ages of 18 and 85 years can open an NPS account. The applicant must comply with Know Your Customer (KYC) norms as stipulated by PFRDA.

NRIs can also invest in NPS, though their contributions are subject to applicable regulatory guidelines and foreign exchange laws.

For government employees, NPS is mandatory and is auto-enrolled at the time of joining service.

For private sector employees and self-employed individuals, it remains a voluntary scheme. There is no income threshold requirement to open an NPS account, making it accessible to individuals across income levels — from daily-wage earners to high-net-worth individuals.

How to Open an NPS Account

Opening an NPS account is a straightforward process available through both online and offline channels.

Online Process:

- Visit DSP Pension

- Enter your PAN details and Aadhaar number for eKYC verification.

- Fill in personal, contact, and other details accurately.

- Choose your Pension Fund Manager and investment scheme preference.

- Make the initial contribution online and Permanent Retirement Account Number (PRAN) will be generated and sent to your registered email/mobile.

NPS Account KYC Verification Process

The KYC (Know Your Customer) process is a mandatory step when opening an NPS account and is designed to verify the identity and address of the subscriber in compliance with regulatory guidelines.

For online registration, Aadhaar-based e-KYC is the most commonly used method. The subscriber's Aadhaar number is linked to their mobile number, and an OTP-based authentication process verifies the identity instantly. Alternatively, CKYC can also be used for identity verification as we can now fetch KYC from central repository of CERSAI.

Features and Benefits of NPS

The benefits of NPS account are wide-ranging, making it one of the most comprehensive retirement savings instruments in India:

• Low-Cost Investment: NPS has one of the lowest fund management charges in the Indian financial market, making it highly cost-effective over the long term.

• Market-Linked Returns: Unlike fixed deposits or PPF, NPS offers market-linked returns with exposure to equities, which can significantly grow the corpus over a long investment horizon.

• Flexible Investment Choices: Subscribers can choose between Active Choice (manual allocation) and Auto Choice (age-based automatic rebalancing).

• Portability: The NPS account (PRAN) is fully portable across jobs, locations, and sectors, making it ideal for the modern mobile workforce.

• Transparency: NAVs (Net Asset Values) of NPS funds are published daily, ensuring complete transparency in fund management. NAV can be checked on NPS Trust Website or directly on Fund Manager’s website.

• Tax Efficiency: NPS offers multiple layers of tax benefits, making it one of the most tax-efficient investment tools available in India.

• Annuity Flexibility: On maturity, subscribers can choose from multiple PFRDA-registered annuity service providers to design a pension plan that suits their needs.

• Partial Withdrawal: Subscribers can partially withdraw up to 25% of their own contribution for specific purposes such as education, medical emergencies, or home purchases etc.

NPS Tax Benefits

One of the most compelling reasons to invest in NPS is the exceptional tax benefit of NPS scheme available under the Income Tax Act, 1961. NPS offers a three-tiered tax advantage that makes it stand out from most other investment options:

• Section 80CCD(1): Contributions up to 10% of salary (for employees) or 20% of gross income (for self-employed) are deductible, subject to the overall Rs. 1.5 lakh limit under Section 80C.

• Section 80CCD(1B): An additional exclusive deduction of up to Rs. 50,000 over and above the Rs. 1.5 lakh limit under Section 80C is available. This makes the total deduction potential Rs. 2 lakh per year.

• Section 80CCD(2): For salaried employees, the employer's contribution to NPS (up to 10% of salary for private sector; 14% for government employees) is also deductible — and this does not fall within the Rs. 1.5 lakh cap.

Furthermore, 60% of the NPS corpus withdrawn at maturity is completely tax-free, adding another layer of tax efficiency. Only the annuity income received post-retirement is taxable as per the applicable income tax slab.

NPS Returns and Interest Rate

Unlike traditional savings instruments, NPS does not offer a fixed interest rate. Instead, returns are market-linked and depend on the performance of the underlying asset classes — equities, corporate bonds, and government securities — in which the contributions are invested.

Historically, NPS equity funds (Tier 1, Scheme E) have delivered returns in the range of 10% to 12% per annum over a 10-year period, while government securities and corporate bond funds have returned approximately 8% to 10% per annum. The blended returns across a diversified NPS portfolio have historically ranged between 9% and 11% per annum, outperforming several traditional fixed-income instruments like PPF and fixed deposits over comparable periods.

It is important to note that past performance is not a guarantee of future returns, as NPS funds are subject to market risks. However, for long-term investors — those with a 20- to 30-year investment horizon — the power of compounding, combined with disciplined equity exposure, can create a substantial retirement corpus. PFRDA regularly publishes fund performance data, allowing subscribers to track and compare returns across different fund managers and make informed decisions.

How to Check Your NPS Balance and Login

Tracking your NPS account balance and investment performance is simple and can be done online:

• Visit the CRA (Central Recordkeeping Agency) portal.

• Click on 'Login for Subscriber' and enter your PRAN (Permanent Retirement Account Number) or PAN and password.

• Navigate to 'Transaction Statement' or 'Holdings' to view your current corpus, contributions made, and fund NAV details.

• You can also check your NPS balance via the NPS mobile app available on Android and iOS.

• SMS alerts and email notifications are sent for every contribution made, ensuring real-time tracking.

• Annual account statements are also dispatched to registered email IDs, summarizing the year's contributions, returns, and total corpus value.

NPS Withdrawal Rules and Exit Strategy

The NPS has well-defined rules for withdrawal, designed to ensure that a significant portion of the corpus is preserved for generating a regular pension income post-retirement.

Upon reaching the age of superannuation, a subscriber can withdraw up to 60% of the total accumulated corpus as a tax-free lump sum. The remaining 40% must be compulsorily used to purchase an annuity from a PFRDA-registered Annuity Service Provider (ASP). This annuity generates a regular monthly pension for the rest of the subscriber's life.

In case of premature exit — exiting before the age of superannuation — only 20% of the corpus can be withdrawn as a lump sum, and the remaining 80% must be annuitized. However, if the total corpus is Rs. 5 lakh or less, the subscriber can withdraw the entire amount as a lump sum without the mandatory annuity purchase.

Partial withdrawals are also permitted for specific purposes: higher education of children, marriage of children, purchase or construction of a residential house, treatment of critical illnesses, and starting a new business. The partial withdrawal limit is capped at 25% of the subscriber's own contributions, and a maximum of three such withdrawals are allowed during the entire NPS tenure.

In the unfortunate event of the subscriber's death, the entire accumulated corpus is paid to the nominee or legal heir without the mandatory annuity requirement, providing financial security to the family.

Frequently Asked Questions (FAQs)

Q1. How many years will NPS pay pension?

NPS pays pension for the lifetime of the subscriber through the annuity plan purchased at retirement. The duration depends on the type of annuity chosen — some plans provide pension only to the subscriber, while others also cover the spouse after the subscriber's death. Essentially, as long as the subscriber (and in joint-life plans, the spouse) is alive, the pension continues.

Q2. Is NPS better than EPF?

Both NPS and EPF (Employees' Provident Fund) serve as retirement savings tools but differ significantly in structure. EPF offers fixed, government-declared returns.

NPS, on the other hand, offers market-linked returns which have historically been higher over the long term, along with greater investment flexibility and additional tax benefits under Section 80CCD(1B). For those seeking higher long-term returns and tax savings beyond the Rs. 1.5 lakh limit, NPS can be a more advantageous choice. A combination of both can be ideal for comprehensive retirement planning.

Q3. What happens to NPS after 60 years?

After reaching 60 years of age, an NPS subscriber can withdraw up to 60% of the total corpus as a tax-free lump sum. The remaining 40% must be used to purchase an annuity from a PFRDA-registered provider, which generates a regular monthly pension for life. Subscribers also have the option to defer the withdrawal up to the age of 85 if they wish to continue accumulating their corpus for a larger retirement benefit.

Q4. Can a 70 year old invest in NPS?

Yes, as per the PFRDA's revised guidelines, individuals up to 85 years of age are eligible to open and invest in an NPS account. This extension was introduced to encourage older citizens to benefit from NPS's tax advantages and structured pension benefits.

Q5. Is NPS pension till death?

Yes, the NPS pension — generated through the annuity purchased at retirement — is paid for the lifetime of the subscriber. Depending on the annuity variant chosen, it can also continue for the spouse's lifetime after the subscriber's death. Some annuity plans also include a return of purchase price to the nominee upon the death of both the subscriber and spouse, ensuring that the family benefits even after the subscriber is no longer alive.

Disclaimer

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns under NPS are subject to market risk and are prone to fluctuation depending on the state of the Financial market.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the schemes of DSP Pension Fund Managers Private Limited. Tax laws are subject to change.