When it comes to building long-term wealth and saving taxes efficiently, investors often find themselves debating NPS vs Mutual Funds. Both are popular investment avenues in India, yet they serve slightly different financial purposes. While NPS is primarily a retirement-focused product, Mutual Funds cater to diverse goals such as wealth creation, tax saving, and liquidity.

In this article, we will break down NPS vs Mutual Funds, compare tax benefits, returns, flexibility, and help you decide what works best for your financial goals.

What is the National Pension System (NPS)?

The Pension Fund Regulatory and Development Authority regulates the National Pension System (NPS), a government-backed retirement savings scheme introduced to encourage disciplined retirement planning. It is a defined contribution scheme; the final pension depends on the accumulated contributions and market performance of underlying assets.

Overview and Purpose of NPS

NPS is a long-term retirement-focused investment product designed to provide financial security after retirement. It was initially launched for government employees and later extended to private-sector employees and self-employed individuals.

The main objective of NPS is to create a retirement corpus through regular contributions during your working years.

Key Features of NPS

• Regulated by PFRDA

• Available to Indian citizens including NRI and OCI aged between 18 to 85

• Offers two account types: Tier I (mandatory retirement account) and Tier II (voluntary savings account)

• Low fund management charges

• Investments are in a mix of Assets- Equity (E), Corporate Debt (C), Government Securities (G). Subscribers can choose their own asset allocation (active choice) or select risk-based lifecycle (auto-choice).

• Rebalancing between funds without liquidation of portfolio.

• Partial withdrawal allowed under specific conditions

• Mandatory annuity purchase at retirement if the corpus is over 12 Lakhs

NPS is especially attractive for individuals looking for additional tax deductions beyond Section 80C.

What is a Mutual Fund?

A mutual fund is a pooled investment vehicle that collects money from investors and invests in stocks, bonds, or other securities. These funds are managed by professional fund managers under the supervision of Securities and Exchange Board of India (SEBI).

Overview and Purpose of Mutual Fund

Mutual Funds aim to provide capital appreciation, income generation, or both, depending on the fund type. They can be used for short-term or long-term financial goals such as buying a house, funding education, or retirement planning.

Many investors compare NPS vs SIP, since SIP (Systematic Investment Plan) is a popular method of investing in Mutual Funds regularly.

Key Features of Mutual Fund

• Professionally managed portfolios

• Wide range of categories (equity, debt, hybrid, ELSS, index funds)

• High liquidity (except ELSS with 3-year lock-in)

• Flexible investment via lump sum or SIP

• Market-linked returns

• No mandatory annuity purchase

• Tax on capital gains based on long term or short-term investments

When analyzing SIP vs NPS, flexibility and liquidity become major differentiators.

Key Features of NPS and Mutual Fund

Investment Options in NPS

NPS allows investors to invest in schemes launched under Multi Scheme Framework (MSF) and in common schemes. Under common scheme they can choose between:

• Active Choice – Decide allocation among Equity, Corporate Debt, Government Securities

• Auto Choice – Allocation adjusts automatically based on age

Equity exposure in NPS is capped (generally up to 75% for private investors), reducing aggressive risk.

Investment Options in Mutual Fund

Mutual Funds offer diverse categories:

• Equity Funds (large-cap, mid-cap, small-cap)

• Debt Funds

• Hybrid Funds

• ELSS (tax-saving Mutual Funds)

• Index Funds and ETFs

In the debate of Mutual Funds vs NPS, Mutual Funds clearly offer broader diversification options.

Tax Benefits in both NPS and Mutual Fund

NPS Tax Benefits:

• ₹1.5 lakh under Section 80C

• Additional ₹50,000 under Section 80CCD(1B)

• Employer contribution up to 10% to 14% of salary deductible under 80CCD(2)

Mutual Fund Tax Benefits:

• ELSS eligible under Section 80C (₹1.5 lakh limit)

• Long-term capital gains (LTCG) taxed at 10% above ₹1 lakh in equity funds

When comparing NPS vs Mutual Funds purely from a tax deduction perspective, NPS provides an extra ₹50,000 benefit.

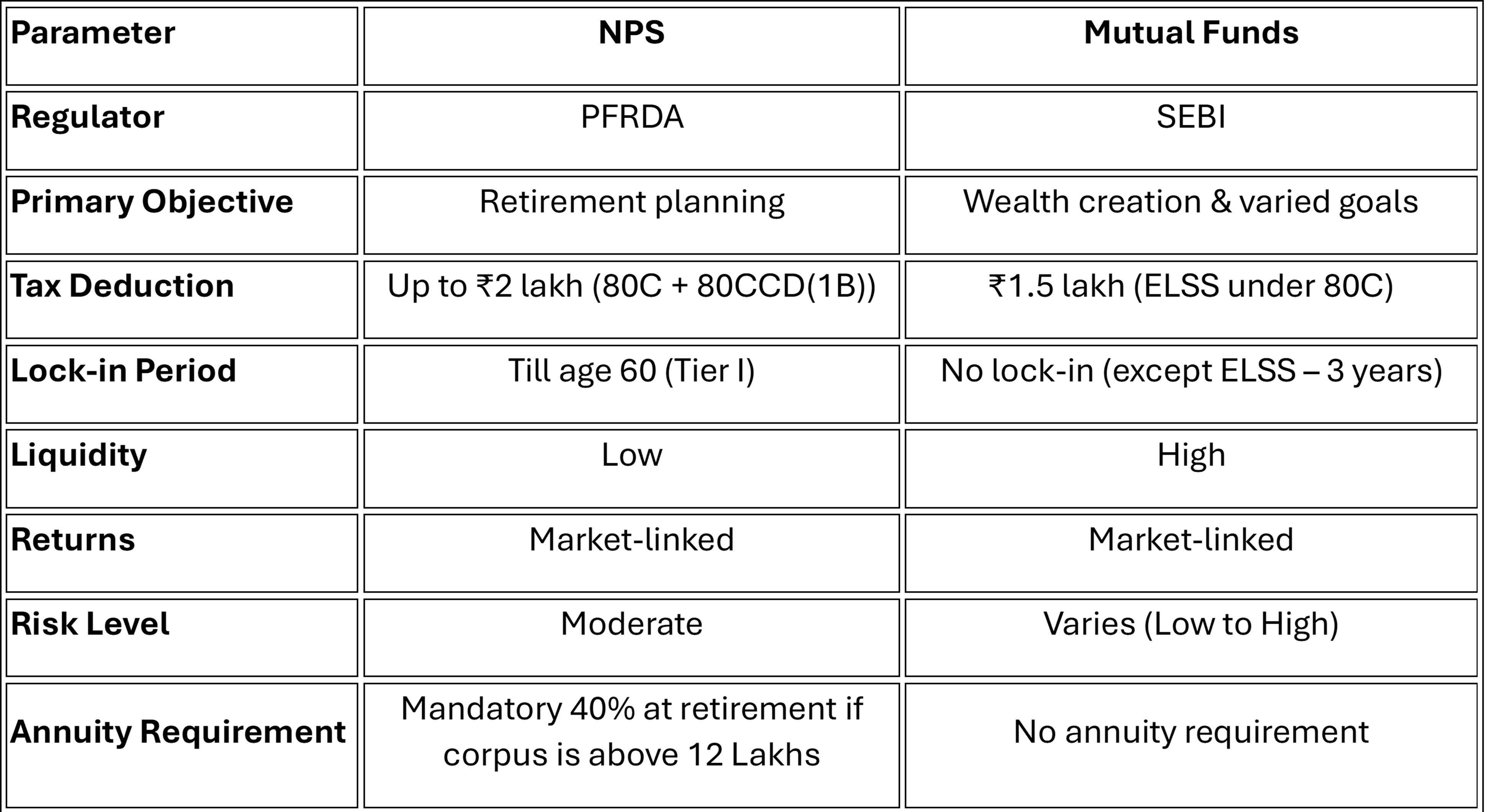

NPS vs Mutual Fund: A Direct Comparison

Tax Deductions and Exemptions

In NPS vs Mutual Funds, NPS wins in terms of additional tax deduction under Section 80CCD(1B). Mutual Funds (ELSS) only qualify within the 80C limit.

Lock-In Period and Withdrawal Rules

NPS Tier I has a long lock-in until 15 years or the retirement age. Partial withdrawals are allowed under specific conditions. Mutual Funds offer high liquidity, making them suitable for medium-term goals.

Returns and Growth Potential

When evaluating SIP vs NPS, on returns one must keep in mind that returns in NPS is a byproduct of the asset allocation selected by the investor. Hence a direct comparison might not be fair.

Returns in Mutual Funds too depends on the kind of fund (Equity, Hybrid, Debt etc)

Equity funds often offer higher growth potential due to greater equity exposure and no cap. However, NPS may provide stable long-term growth with lower expense ratios.

Long-Term Financial Goals and Retirement Planning

For retirement-specific goals, NPS offers disciplined investing and forced annuitization. For broader wealth creation, Mutual Funds are more flexible.

Risk and Return Considerations

In the discussion of NPS vs SIP, SIP investments in aggressive equity funds may carry higher short-term volatility. NPS gives the choice to balance equity and debt allocation, reducing extreme fluctuations.

Final Verdict: Which is the Better Tax Saver?

The choice between NPS vs Mutual Funds depends on your financial goals.

• If your primary objective is retirement planning with extra tax savings, NPS is highly efficient due to the additional ₹50,000 deduction.

• If you want flexibility, liquidity, and potentially higher growth, Mutual Funds—especially through SIP—are better suited.

Ideally, the smartest approach isn’t choosing SIP vs NPS, but combining both. Use NPS for disciplined retirement planning and Mutual Funds for wealth creation and short-to-medium-term goals.

A diversified strategy often delivers the best financial outcome.

FAQs

Can I invest in both NPS and Mutual Funds simultaneously?

Yes, you can invest in both. Many investors use NPS for retirement tax benefits and Mutual Funds for wealth growth and liquidity.

Which offers better tax benefits: NPS or Mutual Funds?

In Mutual Funds vs NPS, NPS offers additional tax deduction of ₹50,000 under Section 80CCD(1B), making it slightly more tax-efficient.

What are the risks involved in NPS compared to Mutual Funds?

NPS has capped equity exposure, reducing volatility. Mutual Funds, especially small-cap or sector funds, can carry higher risk but also higher return potential.

Are the returns from NPS guaranteed like Mutual Funds?

Neither NPS nor Mutual Funds offer guaranteed returns. Both are market-linked investments.

Can I withdraw from NPS before retirement like a Mutual Fund?

Yes. NPS Tier I has limited partial withdrawals and the feature to pre exit.

Mutual Funds allow redemption anytime (except ELSS lock-in).

If you’re planning long-term financial growth, understanding the differences in NPS vs Mutual Funds, analyzing NPS vs SIP, and comparing SIP vs NPS carefully will help you build a balanced and tax-efficient portfolio.

Disclaimer

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns under NPS are subject to market risk and are prone to fluctuation depending on the state of the Financial market.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the schemes of DSP Pension Fund Managers Private Limited. Tax laws are subject to change.