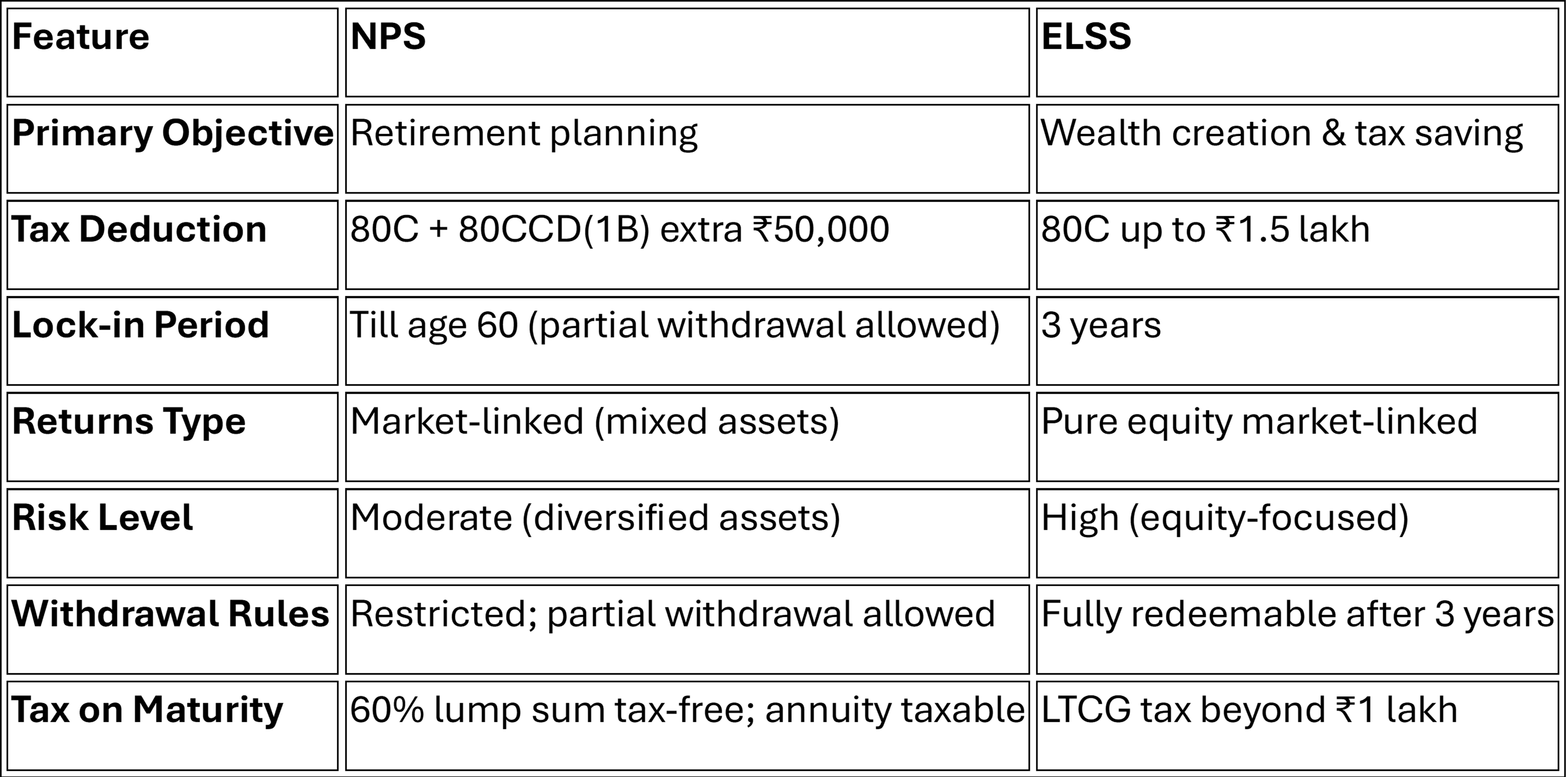

When it comes to tax saving investments in 2026, two popular options dominate the discussion — NPS vs ELSS. Both offer tax benefits under Section 80C (and beyond), but they serve different financial goals. While one is retirement-focused and disciplined, the other is market-linked and flexible.

If you are confused between ELSS Vs NPS, this detailed guide will help you understand the difference between NPS and ELSSso you can make the right choice for your financial planning.

What is the National Pension Scheme (NPS)?

The National Pension System (NPS) is a government-backed retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It was introduced to provide long-term retirement security to Indian citizens.

Overview and Purpose of NPS

NPS is primarily designed to help individuals build a retirement corpus through disciplined, long-term investing. It encourages systematic savings during your working years so you can receive a pension post-retirement.

It is open to salaried employees, self-employed individuals, and even corporate employees through employer contributions.

Key Features of NPS

- Two Types of Accounts – Tier I (mandatory retirement account with restrictions) and Tier II (voluntary savings account).

- Auto & Active Choice – You can choose your asset allocation or let it adjust automatically with age.

- Market-Linked Returns – Invests in equity, corporate bonds, and government securities.

- Low Fund Management Charges – One of the lowest-cost retirement products.

- Tax Benefits Beyond 80C – Offers additional tax deduction up to Rs 50,000 under Section 80CCD(1B). Along with this benefit, salaried employees can save more with Corporate NPS where employer contributes up to 10% to 14% of basic salary depending on old or new tax regime.

NPS is ideal for investors seeking disciplined retirement planning with tax efficiency.

What is ELSS (Equity Linked Savings Scheme)?

An Equity Linked Savings Scheme (ELSS) is a type of diversified equity mutual fund that qualifies for tax deduction under Section 80C of the Income Tax Act.

Overview and Purpose of ELSS

ELSS primarily focuses on wealth creation through equity investments while offering tax-saving benefits. Unlike NPS, it is not specifically meant for retirement — it is a general wealth-building instrument.

Key Features of ELSS

- Equity-Focused Investment – At least 80% invested in equities.

- Shortest Lock-In under 80C – Only 3 years

- SIP Option Available – Invest monthly or lump sum.

- High Growth Potential – Suitable for long-term capital appreciation.

- Capital Gains Tax – LTCG tax applicable beyond ₹1 lakh gains.

ELSS suits investors looking for higher returns and shorter lock-in for tax-saving.

Key Features of NPS and ELSS

Investment Options in NPS

NPS allows investment across:

• Equity (E)

• Corporate Bonds (C)

• Government Securities (G)

Investors can choose asset allocation actively or opt for lifecycle-based automatic allocation.

Investment Options in ELSS

ELSS invests mainly in:

• Large-cap stocks

• Mid-cap stocks

• Multi-cap diversified portfolios

Returns depend entirely on equity market performance.

Tax Benefits in Both NPS and ELSS

• ELSS: Deduction up to ₹1.5 lakh under Section 80C.

• NPS:

o ₹1.5 lakh under Section 80C

o Additional ₹50,000 under Section 80CCD(1B)

o Employer contribution deductible under Section 80CCD(2)

Clearly, from a tax-saving perspective, NPS offers higher total deduction limits.

NPS vs ELSS: A Direct Comparison

Tax Deductions and Exemptions

In the debate of NPS vs ELSS, tax efficiency is key.

NPS provides:

• ₹1.5 lakh under 80C

• ₹50,000 extra under 80CCD(1B)

• Employer contribution deduction

ELSS only qualifies under 80C.

When comparing ELSS Vs NPS, tax benefits are broader in NPS due to additional deductions. However, ELSS provides tax-efficient long-term capital gains (₹1 lakh exemption annually).

Both have different tax treatment structures, so your choice depends on income slab and financial goals

Read more: Old vs New Tax Regime

Lock-In Period and Withdrawal Rules

The biggest difference between NPS and ELSS lies in liquidity.

• ELSS: 3-year lock-in; flexible after that.

• NPS: Vesting period of 15 years or the retirement age; partial withdrawal allowed 4 times for specific reasons.

ELSS wins in liquidity. NPS wins in retirement discipline.

Returns and Growth Potential

ELSS invests primarily in equities, so it has higher volatility but higher long-term return potential.

NPS offers balanced exposure across equity and debt, leading to relatively stable but moderate returns under common schemes. With the introduction of Multi scheme Framework, investor can now select schemes with 100% equity investment.

Both ELSS and NPS may generate similar growth in the future. However if you prefer stability with tax benefits, NPS may suit you better.

Long-Term Financial Goals and Retirement Planning

NPS is specifically built for retirement income through annuity. ELSS is suitable for medium-to-long-term wealth creation goals like buying a house, children’s education, etc.

If retirement planning is your primary concern, NPS is structurally superior

Risk and Return Considerations

ELSS carries full equity risk — suitable for long-term investors comfortable with volatility.

NPS allows controlled equity exposure both in auto and active choice. As age increases, equity exposure reduces automatically.

Read more - Active Choice vs Auto Choice in NPS

The answer to NPS vs ELSS depends on your objective:

• Choose NPS if:

o You want additional ₹50,000 tax deduction.

o Retirement planning is your priority.

o You prefer disciplined, long-term investing.

• Choose ELSS if:

o You want shorter lock-in.

o You seek higher equity-driven returns.

o You need flexibility after 3 years.

For many investors in 2026, a combination of both works best — ELSS for growth and NPS for retirement security.

Understanding the difference between NPS and ELSS ensures you align tax savings with your life goals.

FAQs

Which one is better, NPS or mutual fund?

ELSS (a type of mutual fund) is better for wealth creation and shorter lock-in. NPS is a product for retirement planning and additional tax benefits.

Can I exit from NPS after 5 years?

Partial withdrawal is allowed after 4 times for specific reasons. Full exit before 60 can be done, if the total fund accumulated in less than of equal to 5 Lakhs then investor can exit and withdraw the full amount. However, if the funds are higher then only 20% can be withdrawn tax free and rest goes towards buying annuity.

Is NPS good for tax savings?

Yes. NPS provides deduction under 80C plus additional ₹50,000 under 80CCD(1B), making it highly tax efficient.

Is NPS better than ELSS?

NPS is better for tax saving and income on retirement. ELSS is better for higher growth and liquidity.

Can I claim NPS in both 80C and 80CCD?

Yes. NPS contributions qualify under 80C (up to ₹1.5 lakh) and additional ₹50,000 under Section 80CCD(1B).

If you are planning your tax-saving strategy for 2026, evaluating NPS vs ELSS carefully will help you make a smarter financial decision aligned with your goals.

Disclaimer

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns under NPS are subject to market risk and are prone to fluctuation depending on the state of the Financial market.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the schemes of DSP Pension Fund Managers Private Limited. Tax laws are subject to change.